How a firm articulates and communicates its purpose is increasingly a focus for the FCA as it carries out its supervisory activity. It will look at the purpose of a firm to understand what the firm is trying to achieve in practice rather than simply reading what it written down in the mission statement, and, it will test if staff understand the what the written down purpose of the firm is.

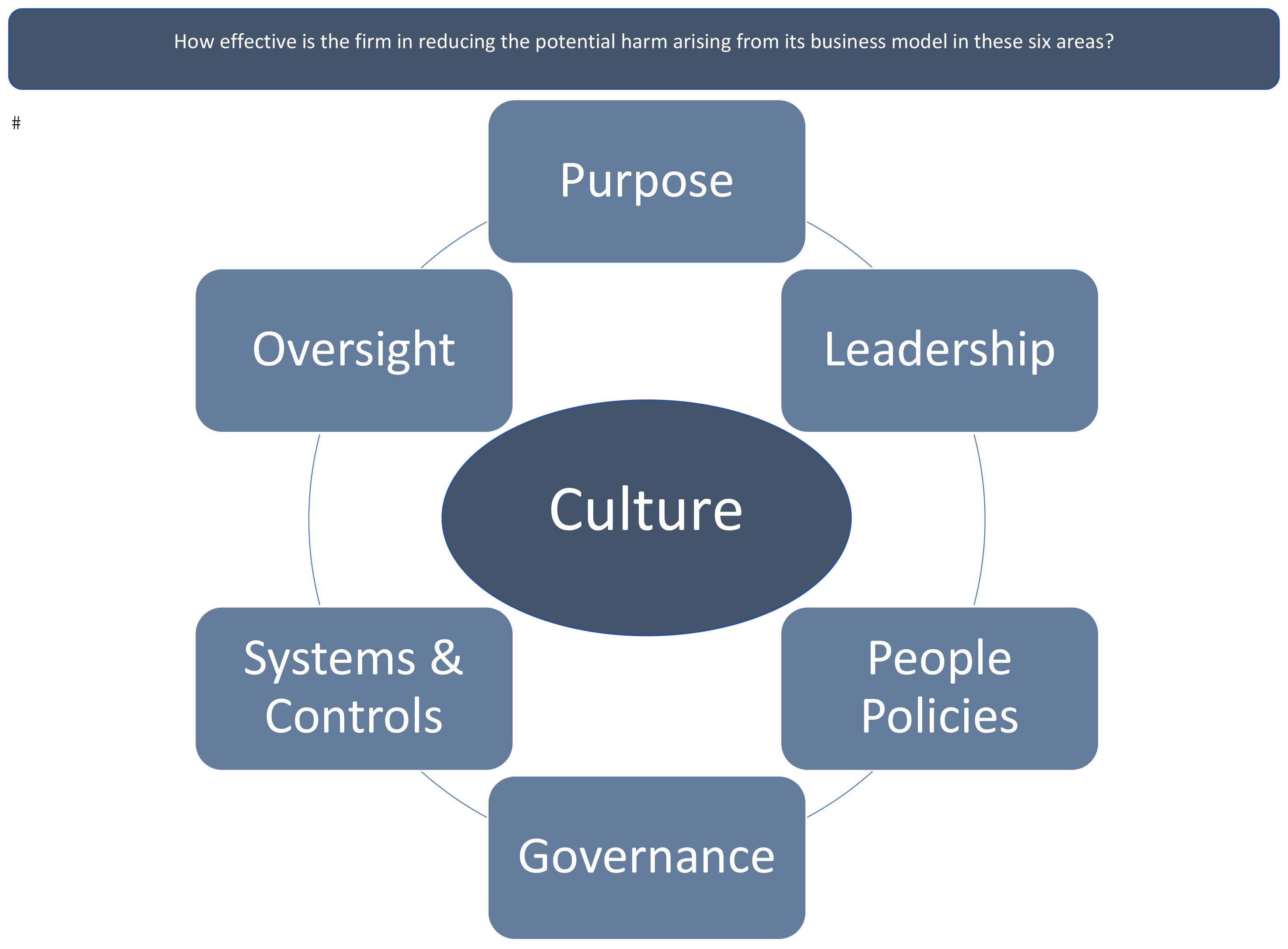

In a recent update to a paper on culture and governance published on its website, the FCA states: “We define culture as the habitual behaviours and mindsets that characterise an organisation. We do not attempt to assess mindsets and behaviours directly; instead we recognise that there are many drivers of behaviour which firms can identify and manage. As a regulator, we focus on 4 key drivers which we believe can lead to harm:

- Purpose

- Leadership

- Approach to rewarding and managing people

- Governance

Through our supervision of firms, we determine how effective each of these drivers of behaviour are in reducing the potential harm arising from a firm’s business model”.

They will want to see the business driving good customer outcomes and that customers and the market are at the heart of way a business is run

In its document FCA Mission: Approach to Supervision, the regulator also states, under the heading Focus on culture and governance: “We look at what drives behaviour in a firm. We address the key drivers of behaviour which are likely to cause harm. These include the firm’s purpose (as it is understood by its employees), the attitude, behaviour, competence and compliance of the firm’s leadership, the firm’s approach to managing and rewarding people (e.g. staff competence and incentives), and the firm’s governance arrangements, controls and key processes (e.g. for whistleblowing or complaint handling)”.

But what is the purpose of a business? We will explore a business definition of purpose and link it to FCA expectations.

The Purpose of a Firm

The purpose of a financial services firm is to offer value through advisory or discretionary management services to clients or customers, who pay for the value. The money received should fund the costs of operating the business as well as provide an income to the owners and dividends to shareholders. Any money in excess of funding and salaries, i.e. profit, may be used to reinvest in the business for future needs or set to reserves.

While job titles may change over time, essentially, we are advising our clients which is the most suitable insurance, protection or investment product for their needs and how efficiently to use tax wrappers where available.

At the highest level, the firm’s mission statement could lend itself to a marketing strapline e.g., ‘never knowingly undersold’ or ‘every little helps’ and we immediately know the two retailers who have used those. To articulate the purpose of your business you need to consider its actual impact on your clients or customers and it will define what it is you offer them.

If we break this down, the purpose of a business has been defined as “an organisation’s meaningful and enduring reason to exist that aligns with long-term financial performance, provides a clear context for daily decision making, and unifies and motivates relevant stakeholders.”

This is where the FCA will look for cues that inform how the culture and governance of your firm will meet the 11 principles for business (found in PRIN) and the conduct rules (in COCON) as they apply to both individuals (of which there are five rules) and senior managers (who have an additional four to comply with). They will want to see the business driving good customer outcomes and that customers and the market are at the heart of way a business is run.

What are the Characteristics of Purpose?

If we now break the above definitions into five characteristics, we can see how they may apply to your own business.

- A meaningful reason to exist

This is more than simply selling your service to your clients and customers. It should include the development of employees to help their growth and achievement, and, could include active involvement in the local community for, say, the benefit of disadvantaged groups.

- Purpose forms an organisational identity

It helps the public perception of the business, or its reputation. Do you want your staff to be proud to work for you, do you want your customers to be your advocates? How does your business purpose inform your business strategy?

- Purpose and profits

As we have seen above, without profits, the business would cease to exist no matter how laudable the purpose. You need profits to drive the business forwards, but these profits could be a direct result of the purpose of the business.

- A clear context for decision makers

This is the area the FCA will focus on. A carefully articulated purpose will provide key decision makers with clear guidelines regarding the values of the business. The regulator will expect these to be applied consistently on a daily basis.

- Unifying and challenging stakeholders

Articulating your business purpose may challenge stakeholders who may need to change long-held practices. Alternatively, it may bring them together are they strive to achieve a unified purpose.

Putting it into practice

Articulation of the purpose of your business should be the catalyst for building long term value for all stakeholders whether they be the Board, senior managers, staff, customers, or the communities around which your business is based. The FCA will focus its attention on good customer outcomes and your business purpose should support these

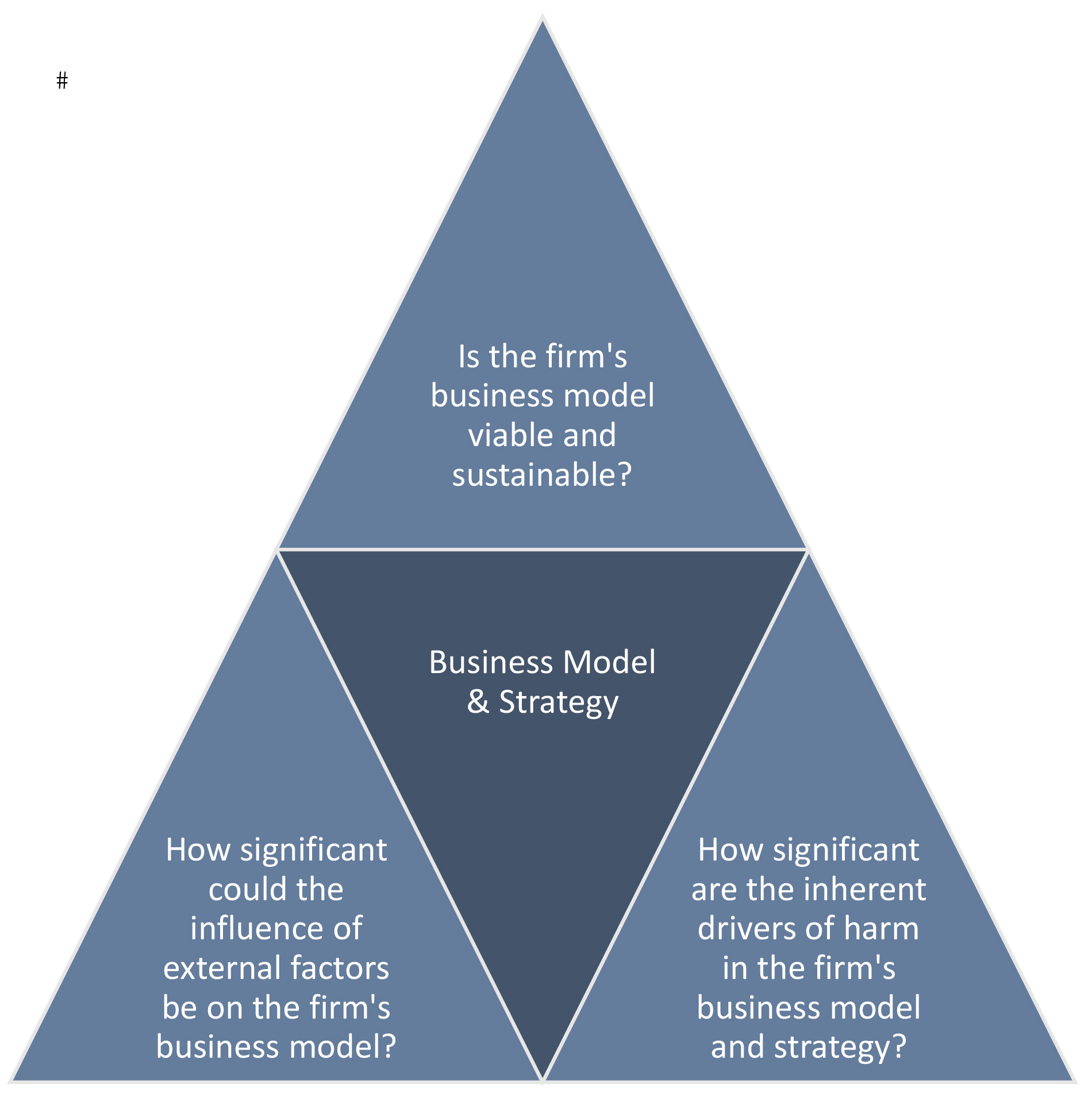

Annex 2 of the FCA Mission: Approach to Supervision document illustrates its Firm Assessment Model in two parts:

- Business model and strategy; and

- Culture.

The diagrams illustrate the questions the FCA will ask your firm in their supervisory work. It would be as well to commence your conversations internally.

{kind=link}