Over the years, the FCA has been fighting a (losing) battle to try to stop consumers receiving poor value and poor advice relating to financial services.

The FCA has tried various different initiatives over the years. These include Treating Customers Fairly (TCF), Retail Distribution Review (RDR), MiFID and MiFID II, Senior Managers & Certification Regime (SM&CR) and now is looking at Consumer Duty – no acronym known at this time.

Most advisers want to do “the right thing”. They act ethically towards their clients and always have. The alphabet soup simply gives them an opportunity to review what they are already doing.

Probably, the most far-reaching initiative was the RDR. It brought in a higher qualification entry point for advisers and also tried to get rid of commission.

My experience is that more qualified advisers tend to be better practitioners because they are more aware of the need to take care with the positive and negative points involved in any advice given and the actions that can be taken.

These issues need to be discovered at the outset of the advice process as that should govern how the adviser treats the client for the remainder of the relationship

Getting rid of commission was rather more difficult. Ideally, the FCA would like advisers to move towards a proper fee structure for services rather than payment for sales. The payment for sales was seen as a route cause of poor advice and poor consumer outcomes.

I can remember meeting an adviser in 2001. Just after I had started my own practice. I wanted to try to work towards a fee structure and was excited when the adviser told me that he only works on fees. Brilliant, what were his rates? Hourly rates? Different for various services? He said that his fees for investments are 3% initial and 0.5% per year ongoing. He spoke with no irony and I am not sure whether he noticed my frustration and disappointment.

So, when RDR raised this issue, it was little surprise that commission and trail commission was re-badged as adviser fees. This still remains important to adviser firms as the more established firms have an income stream and therefore a future re-sale value.

MiFID ii tried to change this a little by making it necessary for advisers to clearly state their charges for reviews and what the clients can expect to receive in their review. A step in the right direction.

Consumer duty is being brought in as in the FCA’s experience, financial services markets do not always work well to provide adequate levels of consumer protection, and competition does not always work effectively in consumers’ interests. Where this happens, consumers may suffer harm.

- find it harder to make an informed or timely decision.

- receive unsatisfactory support from their provider

- buy products and services that are inappropriate for their needs, of inadequate quality, are too risky or otherwise harmful

The FCA wants to bring about a fairer, more consumer‑focused and level playing field in which:

- firms are consistently placing their customers’ interests at the centre of their businesses

- competition is effective in driving market-wide benefits, with firms competing to attract and retain customers based on high standards and customer satisfaction, and innovate in pursuit of good consumer outcomes.

- FCA regulation keeps up with technological change and market developments so that:

- consumers are protected from new and emerging harms, and

- firms can innovate to find new ways of serving their customers with certainty of our regulatory expectations

- firms extend their focus beyond ensuring narrow compliance with specific rules, to also focus on delivering good outcomes for customers

- firms consider the needs of their customers – including those in vulnerable circumstances – and how they behave, at every stage of the product/service lifecycle

- firms continuously learn from their growing focus on and awareness of what their customers experience

- in line with our work on diversity and inclusion, firms act to meet the diverse needs of their customers

- consumers get the products and services they need, which are fit for purpose, provide fair value and do not cause them harm

- consumers understand how to use their products and services and receive the support they need to do so, and

- consumers get prompt and appropriate redress when it is due to them, with reduced misconduct ultimately reducing redress costs

The Consumer Duty will do this, building on our previous interventions in markets and recognising the changing environment for consumers, by:

- explicitly setting a higher standard of care across all retail markets, informed by the FCA work on behavioural biases and vulnerability

- extending rules focused on product governance and fair value, which already exist in certain sectors, across all sectors

- focusing on matters of market practice (eg sludge practice) that interfere in consumer decision making and, by doing so, cause harm

- ensuring firms consider the needs of their customers – including those with characteristics of vulnerability – and how they behave, at every stage of the product or service lifecycle, and

- requiring all firms to focus on good customer outcomes and whether those outcomes are met

The FCA 2021/22 Business Plan set out that improving consumer outcomes through the new Consumer Duty was 1 of 5 consumer priorities. The Consumer Duty also directly informs and supports the other 4.

- Enabling consumer to make effective investment decisions.

- Ensuring consumer credit markets work well.

- Delivering fair value in a digital age.

- Making payment safe and accessible.

Transparency of information is one of the most important issues within consumer duty.

Within the investment world, the Sustainable Finance Directive Regulation (SFDR) has introduced greater need for funds managers and providers to be clearer about the contents of their funds and products. This mainly related to the sustainable finance content of their funds. This is very important to advisers as the advisers are entirely reliant on information provided by the fund managers and providers. Most advisers will not have the time or access to information to confirm whether their original recommendation still remains accurate as far as the sustainable credentials.

There is also greater emphasis on dealing with vulnerable clients. This is far more nuanced than most advisers understand. Most advisers think that vulnerable clients are old people. I think that most advisers have met 85-year-old ladies who are far-better informed than they are and any thoughts of vulnerability would be insulting and patronising.

The FCA definition of vulnerability refers to customers who, due to their personal circumstances, are especially susceptible to harm, particularly when a firm is not acting with appropriate levels of care. Firms should think about vulnerability as a spectrum of risk. All customers are at risk of becoming vulnerable and this risk is increased by

characteristics of vulnerability related to 4 key drivers.

- Health – health conditions or illnesses that affect ability to carry out day-to-day tasks.

- Life events – life events such as bereavement, job loss or relationship breakdown.

- Resilience – low ability to withstand financial or emotional shocks.

- Capability – low knowledge of financial matters or low confidence in managing money (financial capability). Low capability in other relevant areas such as literacy, or digital skills.

Characteristics associated with the 4 drivers of vulnerability

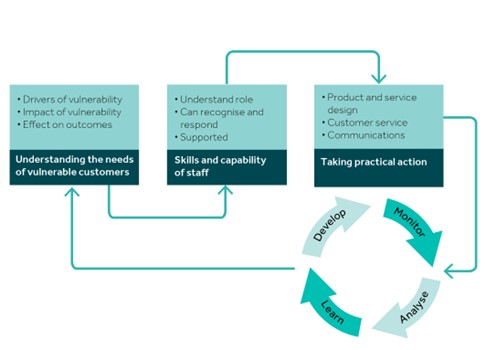

To achieve good outcomes for vulnerable customers, firms should take action to:

- understand the needs of their target market/customer base

- make sure staff have the right skills and capability to recognise and respond to the needs of vulnerable customers

- respond to customer needs throughout product design, flexible customer service provision and communications

- monitor and assess whether they are meeting and responding to the needs of customers with characteristics of vulnerability, and make improvements where this is not happening

The list of vulnerabilities is very long and growing as time goes by. It is now including mental health, stress, and more consideration of personal circumstances, such as bereavement, change of jobs and now insecurity and possibly the onset of personal poverty. The consideration of experience is also necessary. It could be that the clients have no experience or perhaps poor experiences in the past. These issues need to be discovered at the outset of the advice process as that should govern how the adviser treats the client for the remainder of the relationship. It is that identification of vulnerability and then what the adviser has done to accommodate that vulnerability in their behaviour to the client.

So, in order to comply with the new consumer duties, as part of their fact find process, advisers will need to:

- identify any vulnerabilities

- ascertain clients’ social and moral compass to discuss sustainable investment

- their attitude to investment risk and capacity for loss.

- as well as discovering and considering the client circumstances, their objectives and how to achieve those.

As one adviser said to me yesterday “I will not cover all that in 45 minutes”. No, you will not.

The FCA has the ambition that consumers will be less vulnerable when they leave a meeting with an adviser when they walked in or joined the Zoom/Teams Meeting. Their chances of getting a good outcome should be increased.

Is that so much to ask?

{kind=link}