Vulnerability is derived from the Latin word vulnus meaning wound, injury, or emotional hurt. Is it time to find a different word or drop it altogether?

Whether you have clients or customers, I have, for consistency, used the word customer throughout this article.

Coming up for three years ago, the FCA implemented the Consumer Duty. In all of its communications, the FCA has stated that its litmus test of how firms, large and small, have implemented the Consumer Duty will be the treatment of customers with characteristics of vulnerability. The FCA defines vulnerability as:

A vulnerable customer is someone who, due to their personal circumstances, is especially susceptible to harm – particularly when a firm is not acting with appropriate levels of care.

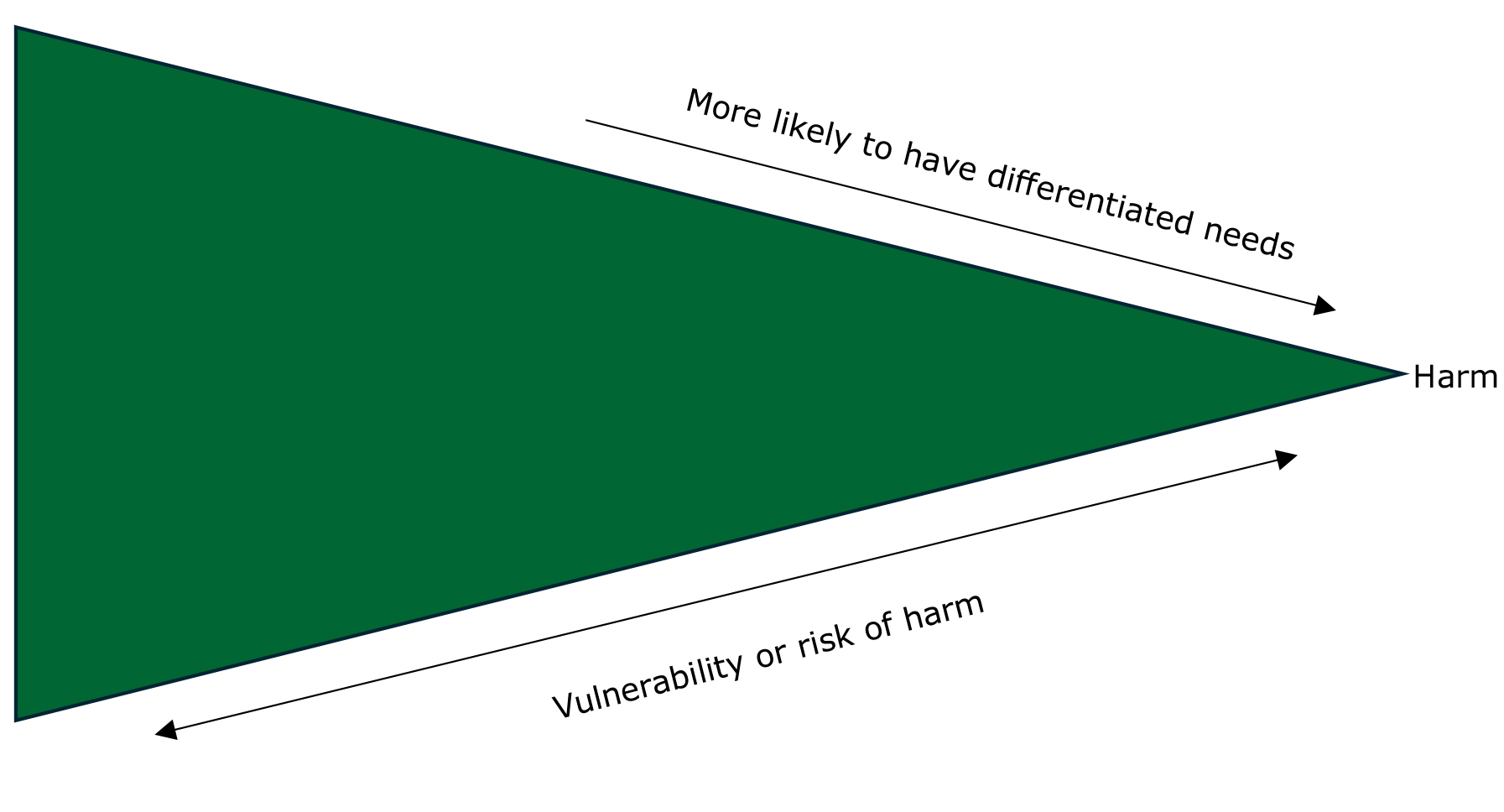

The FCA’s view of vulnerability is as a spectrum of risk with customers moving along the spectrum depending on their individual circumstances. The figure below is based on a similar diagram in FCA Final Guidance FG21/1 Guidance for firms on the fair treatment of vulnerable customers.

The key change from the FCA over the last three years is that customers are described as having ‘characteristics of vulnerability’ as opposed to being ‘vulnerable customers.’

We are all at risk of displaying characteristics of vulnerability, whether temporary, sporadic, or permanent. These could be due to:

- Poor health, such as a physical disability or cognitive impairment;

- A life event, such as retirement or bereavement;

- Low resilience to cope with financial or emotional shocks; and

- Low capability, such as poor literacy or numeracy skills.

During the Covid pandemic and the various lockdowns, loneliness was considered a major driver of vulnerability. Roll that forward to a recently bereaved customer now coping with life alone. Their potential for the risk of harm may stretch long after their bereavement.

Where in these four ‘drivers of vulnerability’ would you put, say, the diagnosis of a dread disease such as cancer, is it poor health, or a life event, or both. Customers with a financial windfall are rarely, if ever, considered to be vulnerable, even though they may not have had access to such a large sum of money before.

The key change from the FCA over the last three years is that customers are described as having ‘characteristics of vulnerability’ as opposed to being ‘vulnerable customers.’

Now, think about your own customers. I was talking to the owner of a firm I work with about the Consumer Duty and vulnerability. He told me that he had no vulnerable customers. I pushed him on the subject, and he then spent the next 15 to 20 minutes describing 10 customers and how he supported them, and who else was involved in the advice process when he felt it appropriate.

Here is a financial adviser with 10 customers with characteristics of vulnerability that he did not view as vulnerable. Here is the reason. They are his customers they require additional support and it is part of the way he works with his customers that he naturally put in place the additional support they need. As he put it, they are my customers, I know them, it is what I do.

Do these customers have characteristics of vulnerability?

Consider these customers. The nature of their requirements may indicate the need for additional care by their adviser. For example, people wanting to arrange:

- access their pension benefits at retirement or partial retirement

- an equity release product

- a mortgage as a first-time buyer

- debt consolidation or further credit

- debt management

- the provision of long-term care

- excessive monetary withdrawals from investments

These could be some indicators of vulnerability, but this is not designed as an exhaustive list. What additional safeguards, as appropriate, would you put in place to ensure fair treatment and good customer outcomes. This will apply to each individual, but where we identify groups of the same people we may established a process aligned to the needs and circumstances of that group.

Customers who are carers

You may have customers who care for loved ones; elderly parents, children (young and older) who have additional needs, or spouses or partners. They may find this positive and rewarding but equally there may be times of stress when your customers who are carers need additional support. It may be they want more time to discuss their financial plans with you. They may have financial difficulties and need some forbearance to ease their situation.

Providing support

When speaking to the customers with characteristics of vulnerability:

- Provide additional opportunities for the customer to ask questions about the information you have provided.

- Continuously seek confirmation that they have understood the information that has been provided.

- Ask if there is anybody with them who is able to assist them. Offer them the opportunity to have a family member or friend present during the conversation.

Vulnerability can be sporadic, temporary, or permanent, there are some signs to look for if your customer has difficulty making decisions or you perceive changes in the way they interact with you. Meet BRUCE:

Behaviour: has their behaviour changed in a way that concerns you.

Remembering: does your customer not remember things you expected them to.

Understanding: are there signs that they do not understand what you are telling them in a way they once did.

Communication: how is your customer communicating with you, are they able to articulate their thoughts?

Evaluation: can your customer process the information you are giving them in a way you are used to.

The IDEA protocol can be used when talking to a customer about their situation or health condition.

Impact – ask what it is that the mental health problem either stops the customer doing (in relation to their financial situation), or what it makes harder for them to. This will help provide insight into both the severity of the condition, and its consequences.

Duration – ask how long the customer has been living with their health problem, as the duration of different conditions will vary. This can inform decisions about the amount of time someone needs to be given to discuss their financial situation.

Episodes – some people will experience more than one episode of poor mental health in their lives. You will need to take such a fluctuating condition into consideration and assess what impact this has in a customer’s decision making.

Assistance – you should consider whether the customer has been able to get any care, help, support, or treatment for their condition. This may help in relation to collecting medical evidence.

Throughout, advisers should keep in mind the steps that would bring about better customer outcomes for their health and wellbeing.

The overall message

The approach you take will vary from individual to individual and the list below is to provoke thought:

- Do not make assumptions.

- In some circumstances, you may decide it would be prudent for customers whose vulnerability is temporary, for example caused by a life event, to have extra time, or have further appointments, before they decide to go ahead with any recommendation. This might be because the customer lacks the capability to decide at that point in time or is faced with an unexpected or complex decision.

- Do not use financial jargon, either written or verbal, and frequently check understanding.

- Offer accompaniment for the customer if they feel additional support would be helpful.

- Consider the communication channels you are using. For example, if the customer is deaf, telephone calls may not be appropriate, depending on their hearing levels. Large print and letters printed on A3 paper may assist the partially sighted.

- Use resources from specialist organisations and/or put the customer in touch with relevant third-party organisations who may be able to assist and can offer support on how the needs of vulnerable customers can be met.

If you identify a customer with the characteristics of vulnerability, you must document the characteristics in your customer file, along with the steps you have taken to assist and provide support.

{kind=link}